WGMaTM: AI-Native PMs, the AI Capital Cycle, and the Product Job Market

What Got My Attention This Month, as a Product Leader

Here’s what got my attention this month — a short list of things I read and watched recently that felt worth pausing on, as a product leader.

This month’s main takeaway: The boundaries are blurring. Between PM and builder. Between software and labor. Between venture appetite and market adoption.

If you work in product, this doesn’t feel temporary. It feels like a new operating environment taking shape.

1/ AI-Native PM on the AI Exponential

One of the more interesting things I saw this month came from Cat Wu, Head of Product for Claude Code at Anthropic: A thoughtful look at how PM teams are adapting their workflows and roadmaps in the face of rapidly evolving LLMs.

There were two ideas in particular that stuck with me.

The first was a familiar-looking Venn diagram that, on the surface, could be easy to dismiss as just another version of the classic product management model. I think that would be a mistake.

What it actually reflects is the real thing happening inside product teams right now: The lines are blurring very quickly.

Tools like Claude Code, Codex, Cursor, OpenClaw, v0, Lovable, and Replit are making it easier for more people to move across the product dev lifecycle. Code is more accessible. Prototyping is faster. Distribution is being reshaped from multiple angles. Tiny teams can do the work that once required much bigger ones.

That doesn’t mean product management disappears, but it is changing. It’s almost shapeshifting.

“The new product management rhythm is rapid experimentation, consistent shipping, and doubling down on what works.”

— Cat Wu, Anthropic

We now have solo founders building real SaaS businesses. We have teams compressing in size while accelerating and expanding in output. We have people spending more time learning agentic tools — and then producing much more, faster.

The second idea was Cat’s framing around ‘side quests.’

“A side quest is a short self-directed experiment you run outside your official roadmap—an afternoon spent prototyping an idea, testing a capability you assumed was out of reach, or just seeing what happens when you push the model harder than you expect to.”

At first glance, that might sound like a modern rebrand of Google’s infamous ‘20% time.’ But what got my attention wasn’t the existence of side projects. It was the implication that, in the right environment, they may matter more than a rigid long-range roadmap.

In fast-moving environments, a side quest is not a distraction. It’s not a once-a-year hackathon either. It can be a discovery engine.

And done well — which requires the right team, and the right culture — that kind of aligned autonomy may be part of the recipe for continuously shipping actual value. It also helps explain how products or features that initially look peripheral can become strategically important faster than anyone expected.

In some ways, the PM role is changing as fast as the tools. New learning curves are forming in real time.

In other ways, the role has not changed at all.

Judgment. Taste. Decision-making. Influence. Vision. Strategy. Insight. Adaptability. Impact.

That mix is still the core of product management.

The tools are changing. The focus is changing. The lines are blurring.

But the need for people who can see clearly and bet well is not.

As Ben Horowitz put it… “Your only job is right product, right time.”

2/ An Unprecedented Technology Investment Cycle

ARK’s Big Ideas 2026 report includes one of the more striking charts I saw this month: AI software investment, as a share of GDP, starting to resemble the steepest technology investment cycles in history, with the railroad era as one of the few historical comparisons.

ARK also argues that consumers are adopting AI faster than they adopted the internet. That stood out to me because we often talk about AI as if it were a replay of the internet or mobile. It isn’t. This feels so much bigger and faster, with greater intensity.

“As foundation models become a new layer of the internet stack, consumers are interacting less with apps and more through Al agents. That structural shift is activating digital experiences that delight consumers. As a result, consumers are adopting Al at a rate much faster than they did the Internet.”

— ARK Investment Management LLC

And the weird thing is: AI is not just scaling products. It is increasingly helping scale the very work that creates products.

AI is scaling… itself?

Jeremiah Owyang made that point well in his framing around self-scaling AI: agents generating knowledge, coordinating tasks, improving workflows, and reducing the degree to which innovation remains bottlenecked by purely human-paced execution.

“GenAI broke the dependency on human-paced scaling. Agents can generate knowledge, coordinate tasks, and improve workflows continuously, without waiting for us. Growth becomes less constrained by labor, and more constrained by compute, energy, and capital.”

— Jeremiah Owyang

Whether or not we agree with the most aggressive version of that thesis, the direction is hard to ignore: Growth is becoming less constrained by labor alone, and more constrained by compute, energy, and capital.

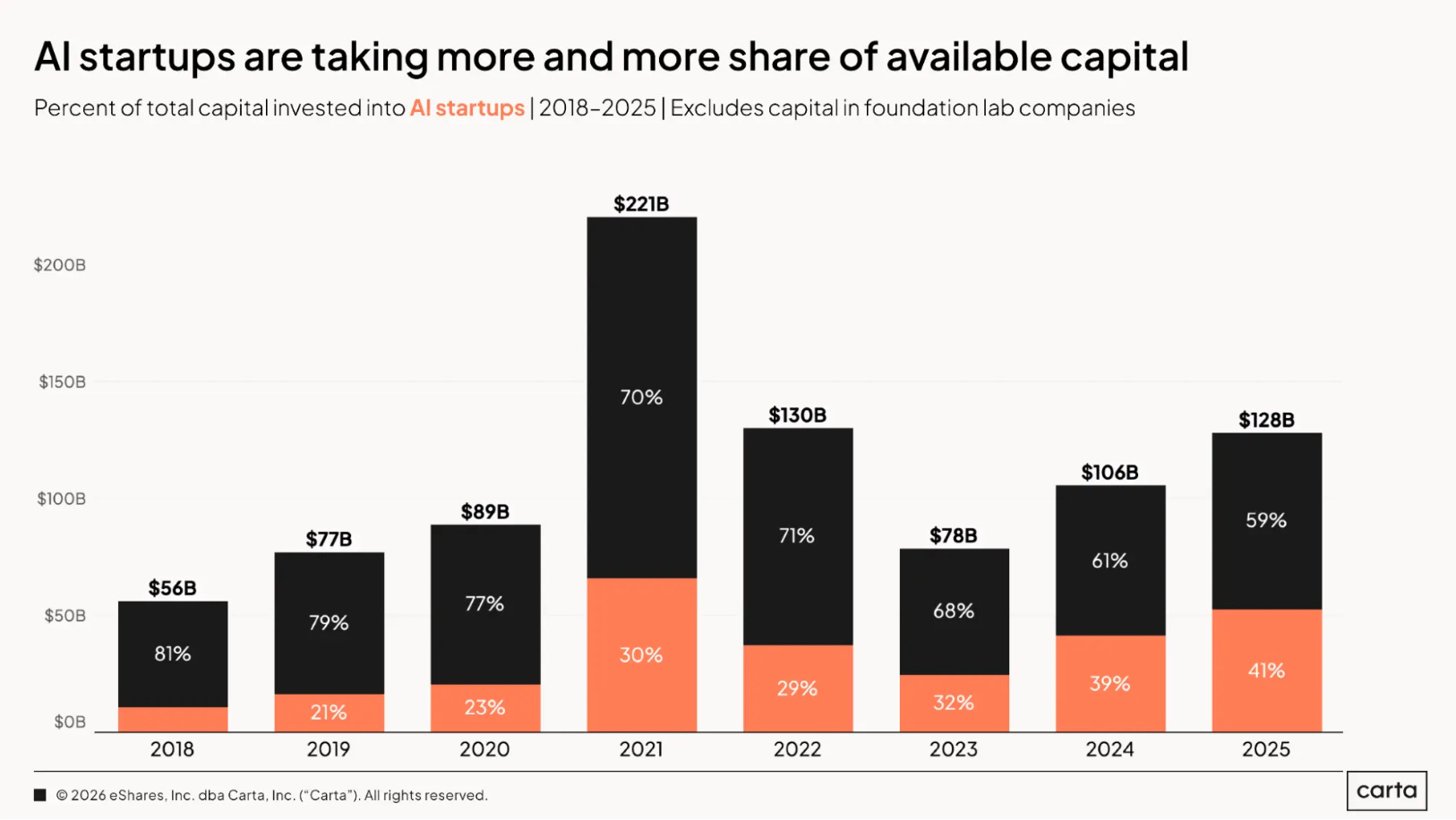

AI is eating VC

According to Carta, AI startups accounted for 41% of the $128 billion in venture dollars raised by companies on Carta last year — a record high annual share.

“This shift in the fundraising market is being driven by changes on both sides of the negotiating table: Venture capitalists are increasingly eager to back AI startups that they believe could one day deliver exponential returns, and startups are increasingly eager to incorporate new AI tools and systems into their business models.”

— eShares aka Carta

That’s venture capital reorganizing itself around AI. Investors are piling into AI so aggressively that a small fraction of startups are capturing an outsized share of funding. And then there are the headline rounds. Billions in funding by OpenAI, Anthropic and xAI is evidence of where the dollars are flowing.

AI is eating software. It’s eating venture. And when that much capital starts clustering around one technological shift, it usually tells us one of two things: Either this is a bubble that will eventually pop, or we are still early in something so significant that we’re struggling to grasp it in real time.

3/ State of the Product Job Market — and Labor Market Impacts of AI

Lenny Rachitsky’s latest State of the Product Job Market showcased some encouraging news:

“There are over 7,300 open PM roles at tech companies globally, and trending up. This is 75% above the low we saw in early 2023, and already up nearly 20% since the start of this year. Today we have the most open PM roles we’ve seen since 2022.”

— Lenny Rachitsky

That does not mean we are back to the post-lockdown surge, when everything in tech seemed to be expanding at once. But it does suggest something important: For all the fear around AI and labor disruption, product hiring has not been frozen. That’s a meaningful sign of resilience.

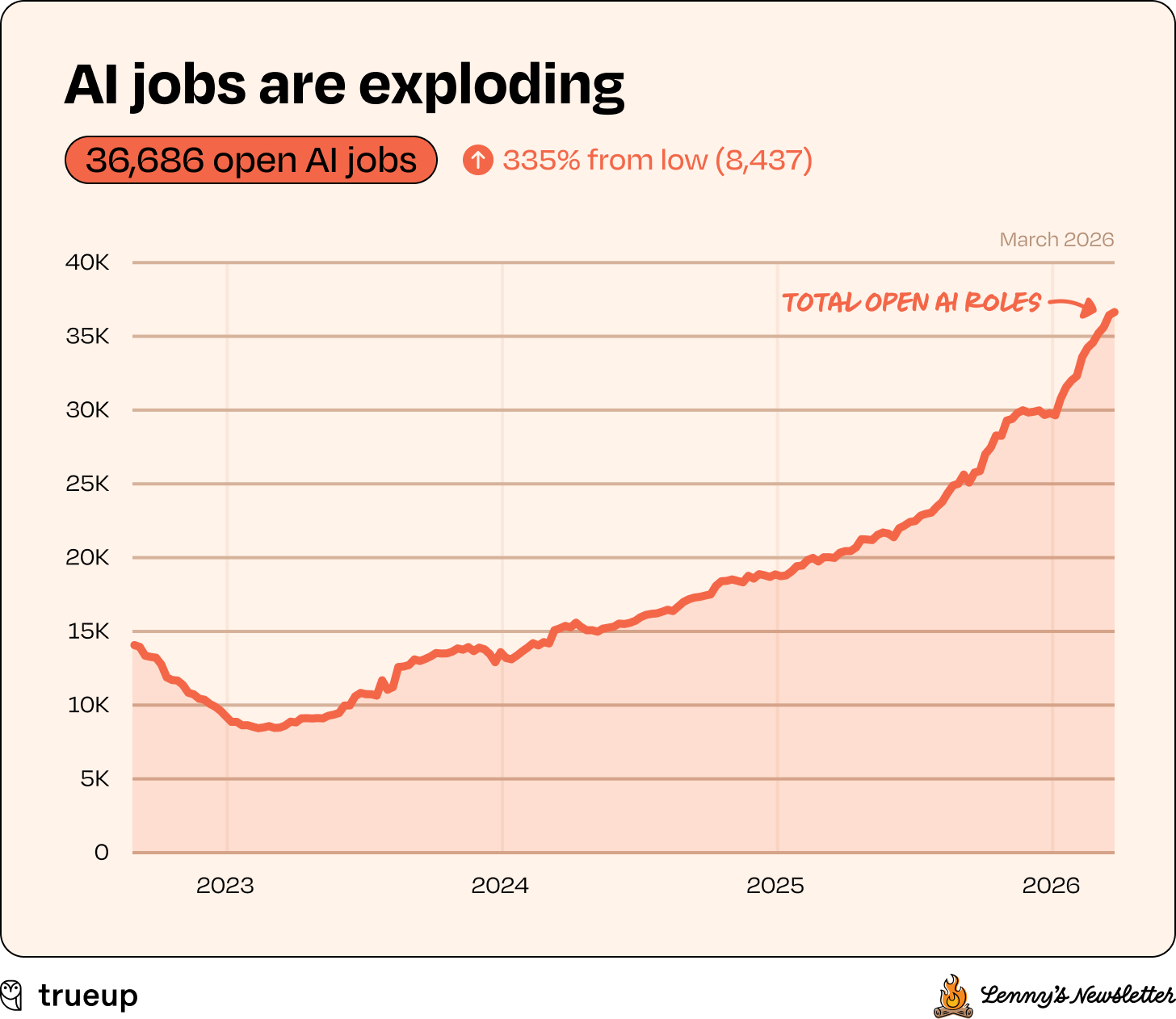

And when it comes to ‘AI jobs,’ we’re seeing hockey-stick growth:

At the same time, Anthropic’s March 5 report on the Labor market impacts of AI added a helpful layer of nuance. Their researchers introduced a new measure of AI displacement risk based not just on theoretical model capability, but on real-world usage patterns.

One of the clearest takeaways: Actual usage is still well below what is theoretically feasible. In other words, AI may be powerful, but the labor market effects are still in relatively early innings.

A few points from that report stood out to me:

‘AI is far from reaching its theoretical capability: actual coverage remains a fraction of what’s feasible’

‘Occupations with higher observed exposure are projected by the BLS (US Bureau of Labor Statistics) to grow less through 2034’

‘Workers in the most exposed professions are more likely to be older, female, more educated, and higher-paid’

‘We find no systematic increase in unemployment for highly exposed workers since late 2022, though we find suggestive evidence that hiring of younger workers has slowed in exposed occupations’

This figure shows the top ten most exposed occupations using their task coverage measure:

“Programmers are at the top, with 75% coverage, followed by Customer Service Representatives, whose main tasks we increasingly see in first-party API traffic. Finally, Data Entry Keyers, whose primary task of reading source documents and entering data sees significant automation, are 67% covered.

At the bottom end, 30% of workers have zero coverage, as their tasks appeared too infrequently in our data to meet the minimum threshold. This group includes, for example, Cooks, Motorcycle Mechanics, Lifeguards, Bartenders, Dishwashers, and Dressing Room Attendants.”

So the job market picture right now is more paradoxical than apocalyptic. There’s demand and movement. There’s also clear signal that the shape of work is changing underneath our feet.

The question for product people is not simply whether these jobs will continue to exist. It’s whether they are learning, adapting, and evolving fast enough to remain unusually useful.

Here’s to the thinkers and builders. Stay resilient.

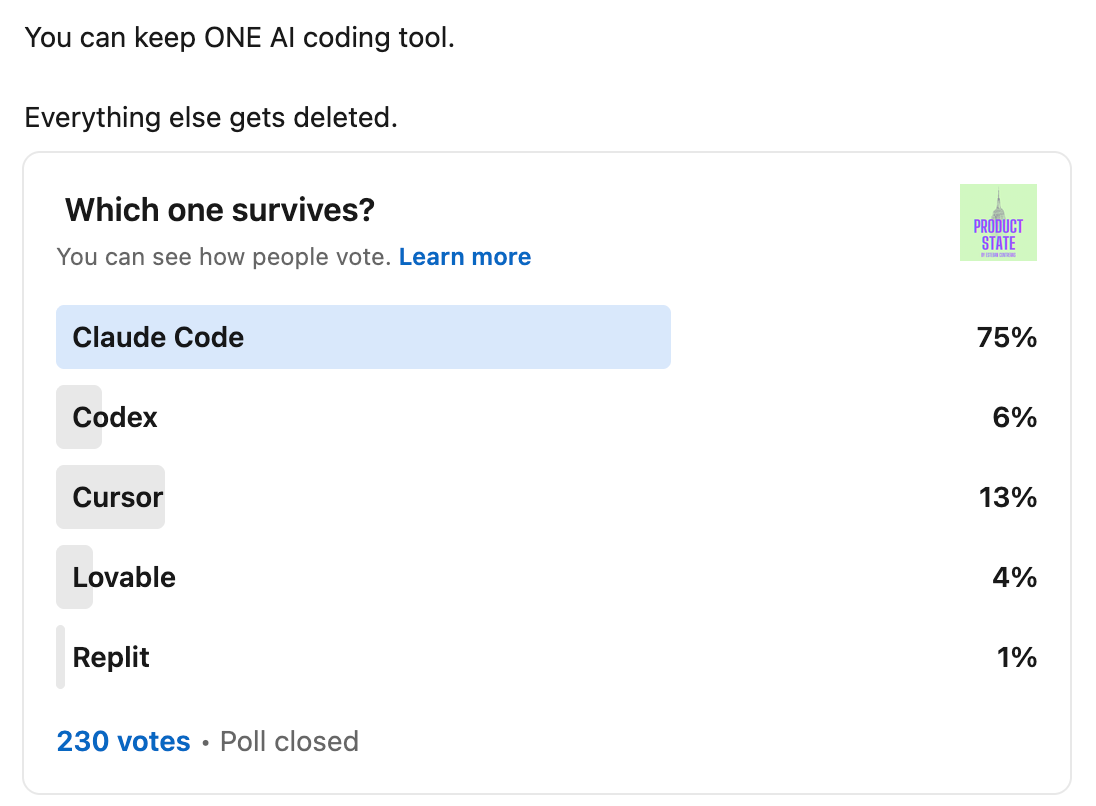

Bonus: Claude Code LinkedIn survey results

A few weeks ago, I asked my LinkedIn network which AI coding tool they’d keep if they could only keep one.

Out of 230 votes, 75% said Claude Code. It wasn’t even close: